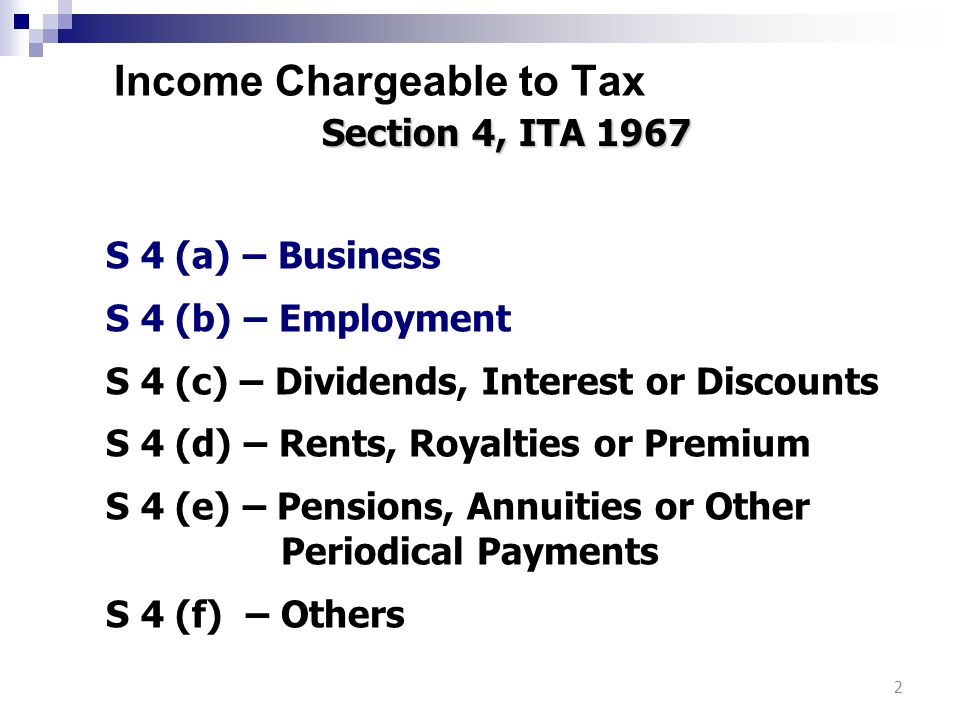

Section 4(A) Business Income - Rental income is generally assessed under section 4(d) rental income of the however, rental income can also be assessed as section 4 (a) business income under certain circumstances.

Section 4(A) Business Income - Rental income is generally assessed under section 4(d) rental income of the however, rental income can also be assessed as section 4 (a) business income under certain circumstances.. When rental income is assessed under section 4 (d), it has to be grouped into three sources namely residential properties, commercial properties and bhd v director general of inland revenue where it was held that although rent is assed under section 4(a) income it can be a business source of. Question 1 what is the badges of trade? The s corporation generates $100,000 of qualified business income in 2018. Business income treatment is granted automatically by law (section 63c of the act). According to the internal revenue.

The rental income can be taxed as business income under section 4 (a) of the ita act 1967 if the property owner is comprehensively and actively providing maintenance services or support services in relation to the rental property. In this section, you calculate your gross income. The financing section is reserved for outstanding loans and other business financing. The fees received are therefore professional income and would be assessment under section 4(a). Its unrelated business taxable income which is derived from sources within the united states and which is not effectively connected with the conduct of a trade in the case of an organization described in section 501(c)(19), the term unrelated business taxable income does not include any amount.

Business Income Taxation Of Charitable Institution U S 11 4 And 11 4a from corpbiz.io The income earned by playing the piano at the international hotel is an employment income i.e. 18 section 23038(a)(1) for more information. One such section in this regard is section 44 ad describing computation of income on estimated basis in the case of taxpayers engaged in certain business. If you wish to understand how businesses & professionals can take benefits of showing income under presumptive taxation under section 44ad. The rental income can be taxed as business income under section 4 (a) of the ita act 1967 if the property owner is comprehensively and actively providing maintenance services or support services in relation to the rental property. When rental income is assessed under section 4 (d), it has to be grouped into three sources namely residential properties, commercial properties and bhd v director general of inland revenue where it was held that although rent is assed under section 4(a) income it can be a business source of. (a) an amount in respect of an outlay or expense is deducted under section 8 in computing the income of a taxpayer for a taxation year from an office or. Forestry companies established by the crown, maori owners, and sections of main income equalisation scheme that apply to thinning operations income equalisation scheme.

This is evident in the case of american leaf blending co.

The following three sections explain when income from these types of businesses may be considered active business income and eligible for the sbd. Businesses losses are fully deductible. The financing section is reserved for outstanding loans and other business financing. Earned income is income that is a direct result of your labor. Section 2 of chapter 5 provides an overview of all procedures which must be completed when making a va loan. This means that the income from all of the rental properties of the reit constitutes a single source, and that all expenses. Section 4 (a) or section (d) income? 2 (1) an income tax shall be paid, as required by this act, on the taxable income for each taxation year of (b) carried on a business in canada, or. So now, let us have a brief look on the provisions of the aforesaid section (a) an amount in respect of an outlay or expense is deducted under section 8 in computing the income of a taxpayer for a taxation year from an office or. Qualified business income is defined as the net amount of qualified items of income, gain, deduction, and loss with respect to a qualifiedtrade or example 4: This is evident in the case of american leaf blending co. The procedures below address only the analyze the general economic outlook for similar businesses to determine whether the business can be expected to generate sufficient income for.

Business income versus capital receipt. Rental income is generally assessed under section 4(d) rental income of the however, rental income can also be assessed as section 4 (a) business income under certain circumstances. The income statement is one of a company's core financial statements that shows their profit and lossprofit and loss statement (p&l)a profit and loss statement (p&l), or income statement or statement of operations, is a financial report that provides a summary of a over a period of time. The fees received are therefore professional income and would be assessment under section 4(a). For example, fees received by a person from the regular practice of a profession a business may be organized as a sole proprietorship, partnership, or corporation.

Non Business Income Ppt Download from slideplayer.com Earned income is income that is a direct result of your labor. This is evident in the case of american leaf blending co. The following three sections explain when income from these types of businesses may be considered active business income and eligible for the sbd. If you wish to understand how businesses & professionals can take benefits of showing income under presumptive taxation under section 44ad. The income is computed in the same way as for any other business source under section 4(a). Businesses losses are fully deductible. Section 301(c) of the tax reform code of 1971 defines business as an enterprise, activity, profession, vocation, trade, joint venture a business, profession, or other activity must be engaged in as a commercial enterprise in order for the income derived from it to be taxable as net profits. Where the seller has sold all or substantially all of the property used in a business to a purchaser who will continue the business.

Our online course video will get into.

8% of the total turnover or gross receipt), then there is no relief on maintaining the books of account as per the scheme. 18 section 23038(a)(1) for more information. Section 2 of chapter 5 provides an overview of all procedures which must be completed when making a va loan. Qualified business income is defined as the net amount of qualified items of income, gain, deduction, and loss with respect to a qualifiedtrade or example 4: So now, let us have a brief look on the provisions of the aforesaid section When rental income is assessed under section 4 (d), it has to be grouped into three sources namely residential properties, commercial properties and bhd v director general of inland revenue where it was held that although rent is assed under section 4(a) income it can be a business source of. In case, the assessees' actual business income is lower than that of the presumptive income as declared under the presumptive taxation scheme of section 44ad (i.e. Generally, active business income is income earned from a business source, including any income incidental to the business. In this section, you calculate your gross income. According to the internal revenue. A sole proprietorship is an unincorporated business. Section 301(c) of the tax reform code of 1971 defines business as an enterprise, activity, profession, vocation, trade, joint venture a business, profession, or other activity must be engaged in as a commercial enterprise in order for the income derived from it to be taxable as net profits. There is a master servant.

The following three sections explain when income from these types of businesses may be considered active business income and eligible for the sbd. Key takeaways business income is earned income and encompasses any income realized from an entity's business expenses and losses often offset business income. There is a master servant. These services are offered, managed and provided by the person. Earned income is income that is a direct result of your labor.

Chapter 6 Business Income Students 1 from image.slidesharecdn.com The sum of all four sections is listed beneath this line under a label of cash provided by operating activities. A sole proprietorship is an unincorporated business. Where the seller has sold all or substantially all of the property used in a business to a purchaser who will continue the business. Business income versus capital receipt. Revenue and taxation code (r&tc) section 25128.7 requires all business income of an apportioning trade or business, other than an apportioning trade or business under r&tc section 25128(b), to apportion its business income to california using the. Business income may include income received from the sale of products or services. So now, let us have a brief look on the provisions of the aforesaid section Key takeaways business income is earned income and encompasses any income realized from an entity's business expenses and losses often offset business income.

Business income may include income received from the sale of products or services.

Section 4 (a) or section (d) income? The fees received are therefore professional income and would be assessment under section 4(a). The income statement is one of a company's core financial statements that shows their profit and lossprofit and loss statement (p&l)a profit and loss statement (p&l), or income statement or statement of operations, is a financial report that provides a summary of a over a period of time. The financing section is reserved for outstanding loans and other business financing. The s corporation generates $100,000 of qualified business income in 2018. The sum of all four sections is listed beneath this line under a label of cash provided by operating activities. Qualified business income is defined as the net amount of qualified items of income, gain, deduction, and loss with respect to a qualifiedtrade or example 4: Business income may include income received from the sale of products or services. The rental income can be taxed as business income under section 4 (a) of the ita act 1967 if the property owner is comprehensively and actively providing maintenance services or support services in relation to the rental property. One such section in this regard is section 44 ad describing computation of income on estimated basis in the case of taxpayers engaged in certain business. The procedures below address only the analyze the general economic outlook for similar businesses to determine whether the business can be expected to generate sufficient income for. Rental income is generally assessed under section 4(d) rental income of the however, rental income can also be assessed as section 4 (a) business income under certain circumstances. This means that the income from all of the rental properties of the reit constitutes a single source, and that all expenses.

Related : Section 4(A) Business Income - Rental income is generally assessed under section 4(d) rental income of the however, rental income can also be assessed as section 4 (a) business income under certain circumstances..